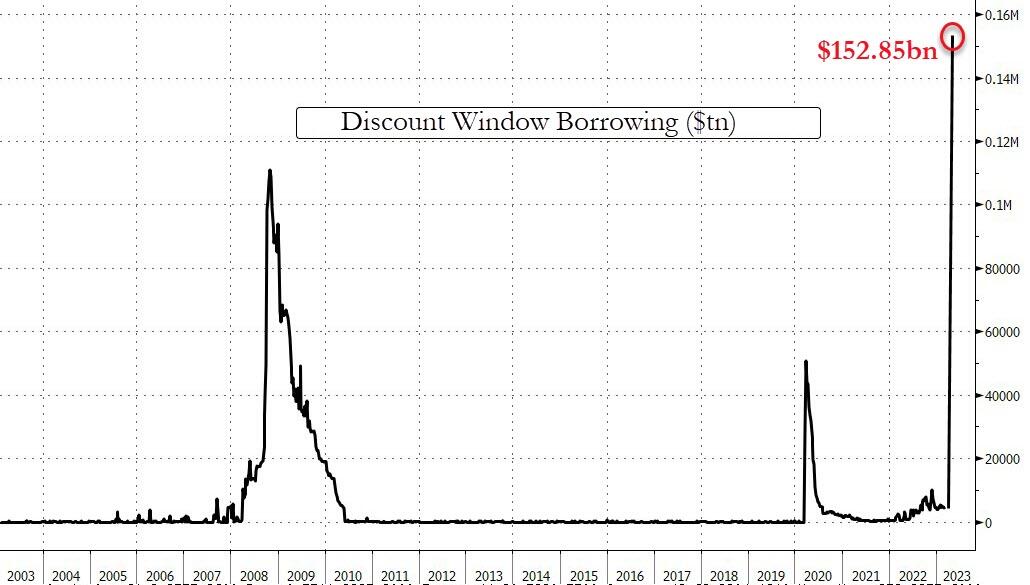

Here’s a trend for you to watch. WOKE banks not being FDIC approved.

View attachment 60595

Nothing ominous about that announcement from Wells Fargo, just a normal disclaimer notification from any bank.

From the FDIC Website:

The FDIC covers

- Checking accounts

- Negotiable Order of Withdrawal (NOW) accounts

- Savings accounts

- Money Market Deposit Accounts (MMDAs)

- Time deposits such as certificates of deposit (CDs)

- Cashier's checks, money orders, and other official items issued by a bank

The FDIC does not cover

- Stock investments

- Bond investments

- Mutual funds

- Crypto Assets

- Life insurance policies

- Annuities

- Municipal securities

- Safe deposit boxes or their contents

- U.S. Treasury bills, bonds or notes*

*These investments are backed by the full faith and credit of the U.S. government.

Depositors do not need to apply for FDIC insurance. Coverage is automatic whenever a deposit account is opened at an FDIC-insured bank or financial institution. If you are interested in FDIC deposit insurance coverage, simply make sure you are placing your funds in a deposit product at the bank.

COVERAGE LIMITS

The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category.

The FDIC provides separate coverage for deposits held in different account ownership categories. Depositors may qualify for coverage over $250,000 if they have funds in different ownership categories and all FDIC requirements are met.

All deposits that an accountholder has in the same ownership category at the same bank are added together and insured up to the standard insurance amount.

WHEN A BANK FAILS

A bank failure is the closing of a bank by a federal or state banking regulatory agency, generally resulting from a bank's inability to meet its obligations to depositors and others. In the unlikely event of a bank failure, the FDIC acts quickly to ensure depositors get prompt access to their insured deposits.

FDIC deposit insurance covers the balance of each depositor's account, dollar-for-dollar, up to the insurance limit, including principal and any accrued interest through the date of the insured bank's closing.

The FDIC acts in two capacities following a bank failure:

- As the "Insurer" of the bank's deposits, the FDIC pays deposit insurance to the depositors up to the insurance limit.

- As the "Receiver" of the failed bank, the FDIC assumes the task of collecting and selling the assets of the failed bank and settling its debts, including claims for deposits in excess of the insured limit.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/Z7VCVZB77JK3HGNX7575QGNG6M.jpg)